📈 Continued Claims

Finance articles often follow the old news trope of “If it bleeds, it leads.” Meaning they cover negative events like recession, inflation, or the “death” of the US dollar to get more clicks. Which we would never do (except last week).

This means that mainstream financial media has been calling for a recession since the middle of last year. To the point where we had to cover it last summer and call it a bunch of garbage.

Now it’s always nice to be right. Even more so when it means the economy didn’t plunge into a horrible recession causing all of you to lose your jobs.

Howeva, that does not mean that bad things can’t happen. And there are some signs (a year later) that recession fears may have some merit. For example, inflation cooling off is decidedly a good thing. But it also means that the economy isn’t running as hot as it was before and people aren’t banging down the door to buy things like they were last year.

Overall, I will gladly trade a little bit of moderation in the name of inflation, but either way, this matters.

On the job front, we largely shut down the myth of layoffs being a huge issue.

Our main point here was that the unemployment rate remained at all time lows despite these doom and gloom headlines. And we stand by that fact and would like to add that the labor market remains historically strong by multiple standards.

But there is a data point called continuing claims that measures how many people continue to file for unemployment. Meaning they got laid off and are unable to find a job, and while this will always be a certain number of people an uptick in this number means layoffs are starting to outpace people finding new positions.

And as you can see here this number has been getting larger since bottoming out in the fall of last year. Just this week we saw the highest print in years which led to a little bit of surprise in the bond market. But as always, context matters.

We are still WELL below all-time highs for claims set during covid and generally in the range that we saw pre-pandemic. And as you can see below we are still in or below the historical range over the last 30+ years so again the alarm bells do not need to go off yet.

The only reason this is concerning is if you pay attention to the above chart, rising continuing claims usually signal a recession. You will notice in the grey areas of 2001, 2008-2009 and the pandemic all had elevated continuing claims that trended higher before the stock market truly bottomed out which we have not seen yet in this post-pandemic cycle.

Now let’s be clear, we are still not saying there is a recession coming anytime soon but these numbers do bear watching right now. So don’t go out and sell all your stocks.

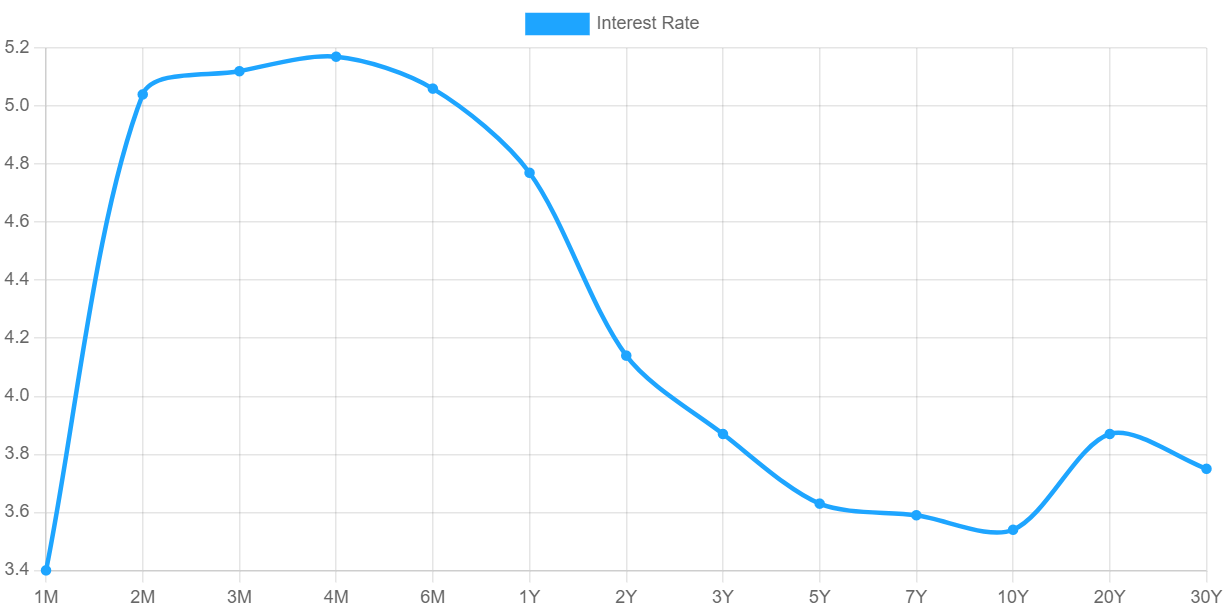

What we are saying is these numbers bear watching, and given a backdrop of cooling inflation and the highest interest rates in decades our old friend the bond market may be a good place to park your money in the coming 6 months to a year.

The easiest way would be via high-yield savings accounts covered here.

And since we published that article Apple has made it even easier to save with this type of product.

In your Roth IRA, you could use a product like SGOV or BIL to invest in short-term government bonds.

And if you are feeling frisky you can invest in government bonds directly through TreasuryDirect.gov locking in high rates for whatever length of time suits your needs.

What’s the Upside?

There is always a data point that will tell you the economy is about to crash if you look close enough. And we are currently monitoring continuing claims as the canary in the coal mine.

But that does not mean you should sell your stocks, especially in your retirement accounts. What it means is you may want to take advantage of high-interest rates in a variety of products to lock in return based on your short-term investment horizon.