Oh My God, It's a Fire... Sale

So far, 2022 has been a rough week month year. With inflation near decade-highs, higher interest rates, wobbly (if not awful) earnings from previous Wall Street darlings, and the total cratering of anything crypto or crypto-adjacent, your experience may best be summarized thusly:

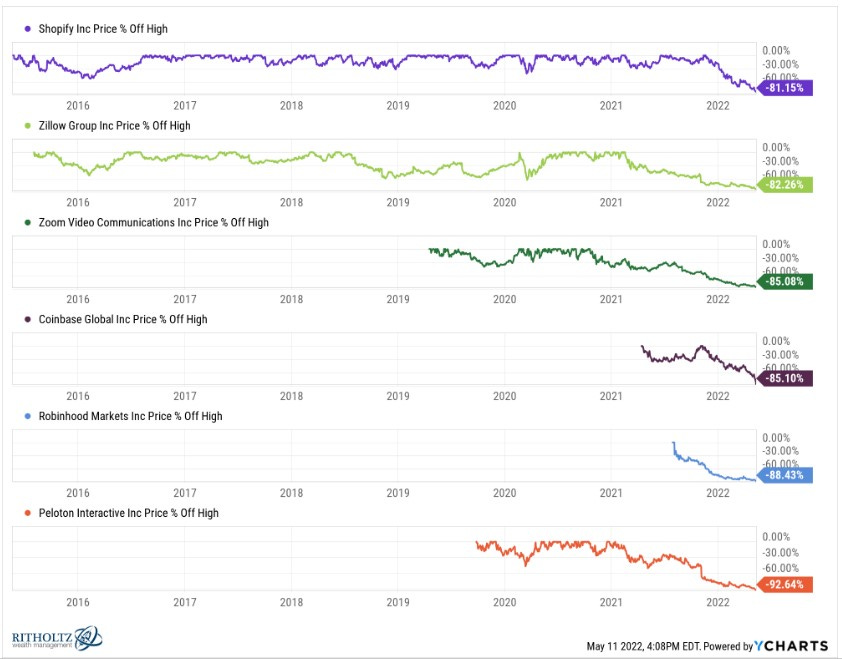

WTF is going on? Well, remember when everyone was all about the WFH trade, buying stocks like Zoom, Peloton, Zillow, Robinhood, and Coinbase? About that:

Each of those names has fallen -81 to -92% from its all-time high price. FAWK. The rest of the market hasn’t fared much better, year-to-date:

Lotsa red there, bud.

It’s not unheard of that the market loses its collective sh*t to start a year and then recover to finish positive on the year. Remember the olden days of 2020? The market fell -34% in March after the COVID-19 lockdowns took effect to finish the year up nearly 16%.

What’s driving the sell-off? Who the f*ck knows what’s truly in the dark hearts of those gutless Wall Street simps, but it sure seems like a lot of it has to do with the Fed (finally) increasing interest rates.

Why does that matter? Well, we know companies like Amazon make gobs and gobs (and gobs and gobs) of money, but, with interest rates at functionally zero for the last decade or so, you don’t pay for stuff out of cashflow. Not when you can leverage that revenue to borrow at a competitive rate and bet that you can outgrow your competitors.

Look at where three of the biggest streaming platforms placed their bets:

Netflix bet its growth on offering subscribers the broadest library of shows - production costs be damned. The thought being that if they had something for everyone, no one would cancel their Netflix subscription.

Disney bet they could quickly add subscribers by leveraging the best IP and deepest content library in the business and practically giving away the product initially (Disney+ is like $8/mo., half the price of Netflix) before raising the price. Also, Indian cricket matters a lot.

Apple bet they could grow AppleTV subscribers by luring existing Apple customers (there are around 1 billion iPhone users around the world - good start) by producing HBO-level shows to compete during awards season, like Ted Lasso or For All Mankind.

Add Amazon Prime Video, HBO Max, Hulu (Disney-owned), Paramount+, Peacock, and on and on into the mix and you get the idea. And these are just the streaming services. Other companies made similar bets (Restoration Hardware borrowed eye-watering amounts of money to turn their showrooms into the “Apple Store for $10k Couches” and it worked).

The party doesn’t last forever. At some point, the companies need to pay down the money they borrowed and/or refinance the debt, something that happens every four to six years, on average. That’s not really a concern if interest rates are falling like they have been for the last 40 years or so.

It’s more of a problem when interest rates are going up and expected to keep going in one direction:

It’s like if you refinanced your super-low <3% mortgage for a 6% mortgage every four to six years. Ouch bruh.

So, Wall Street is pulling a Kim Kardashian: rebalancing away from talented but-kinda-nuts growth companies in favor of… whatever the f*ck Pete Davidson is. He may not make Ye money, but he ain’t poor neither.

So, if we’re in the Pete Davidson market (God help us), does that mean sell everything and sit in cash?

NEWP.

Here’s the reality: if you expect to retire sometime in the 2040s to the 2060s, then you should love this market. For this example, we’re going to assume that you’re pumping money into your 401(k) (or similar: shoutout to the Queen of Queen Creek rocking that 401(a); also, happy birthday) every paycheck.

If that’s the case, then you’re finally – FINALLY – getting to buy some great stocks on sale. See, by regularly contributing to your retirement plan at work, you end up buying the market at different points: sometimes at the highs, sometimes at the lows, and sometimes in the middle. Over decades, it works itself out to be fairly distributed between each moment. So, think of this as the time when you finally get to go discount shopping.

What’s the Upside?

The market may be unnerving, but it’s nothing to worry about just yet. Resist the urge to sell and instead, look at this as an opportunity to finally get a piece of some of them fabric of society companies – like Microsoft, Disney, Amazon, etc. – at a discount. Who doesn’t love a sale?

For Your Weekend

Our round-up of essays, podcasts, and streaming shows to check out over your weekend. We cast a wide net so you don’t have to.

Read:

Average vs. Linear Growth by The Arbitrageur

We have a guest post this week courtesy of friend-of-the-blog The Arbitrageur. Yeah, another pseudonym but that’s cuz he’s a financial advisor affiliated with a national broker-dealer.

The article breaks down how understanding probability can lead to clearer thinking during periods of market volatility (like now). Give it a read!

Listen:

Disney vs. Netflix: The Deathmatch of Streaming (The Town with Matthew Belloni)

You think I got my streaming stats from deep research? If you’re as fascinated by the inner workings of the content machine that is Hollywood as I am, then The Town is required listening.

This episode features an interview with industry analyst Michael Nathanson, who discusses Disney’s latest earnings report discusses whether the cost to potentially beat Netflix in the streaming wars has been worth it.

Follow-up:

We discussed the merits of student loan forgiveness in last week’s newsletter, concluding that outright canceling all student debt goes too far, but doing nothing isn’t tenable either. Our solution is to conditionally stop charging interest on the loans. We also noted that any student loan forgiveness fails to address rapidly rising tuition and administrative costs incurred by students, the root cause for the bloated cost to obtain a college degree.

Senator Chris Murphy (D-CT) echoed the sentiment over the weekend in an appearance on Fox News, saying:

“[The Democratic Party] spends a little bit too much time talking about the debt and not enough time talking about the cost of the degree, because that's where the real problem is… We're going to be in a perpetual cycle of having to forgive debt if college continues to spiral upwards to $100,000 a year."

No word on how to do that just yet. Still we’re heartened to hear some clear thinking on the subject.

Chuckle: