📈Forgive Me Joe Biden, For I Have Borrowed

Student loan forgiveness has been a major plank in the progressive wishlist for years now, enough for Biden to make it part of his successful 2020 presidential campaign. It experienced renewed momentum after the Biden administration extended the moratorium on payments through August 31.

Anytime you talk about “giving” money to one group and not another, someone somewhere in the world gets irrationally angry. Personally, I save my anger to direct it at the Chicago Bears management, but I get the impulse, so let’s look at some of the common arguments against forgiving student loan debt.

I already paid off my loans; why do these kids deserve to get theirs wiped out?

Shut up Boomer

Forgiving loans will create a moral hazard (economist term for encouraging poor behavior), and more people will take out excessive student loans

Bro, people already took out $200k for liberal arts degrees - that ship sailed

Why do only college-educated students get government assistance? What about everyone else?

PPP for small businesses, extended unemployment benefits, billions in farm subsidies, food stamps, etc., etc. Money can and has been handed out. Let’s not act like this is new.

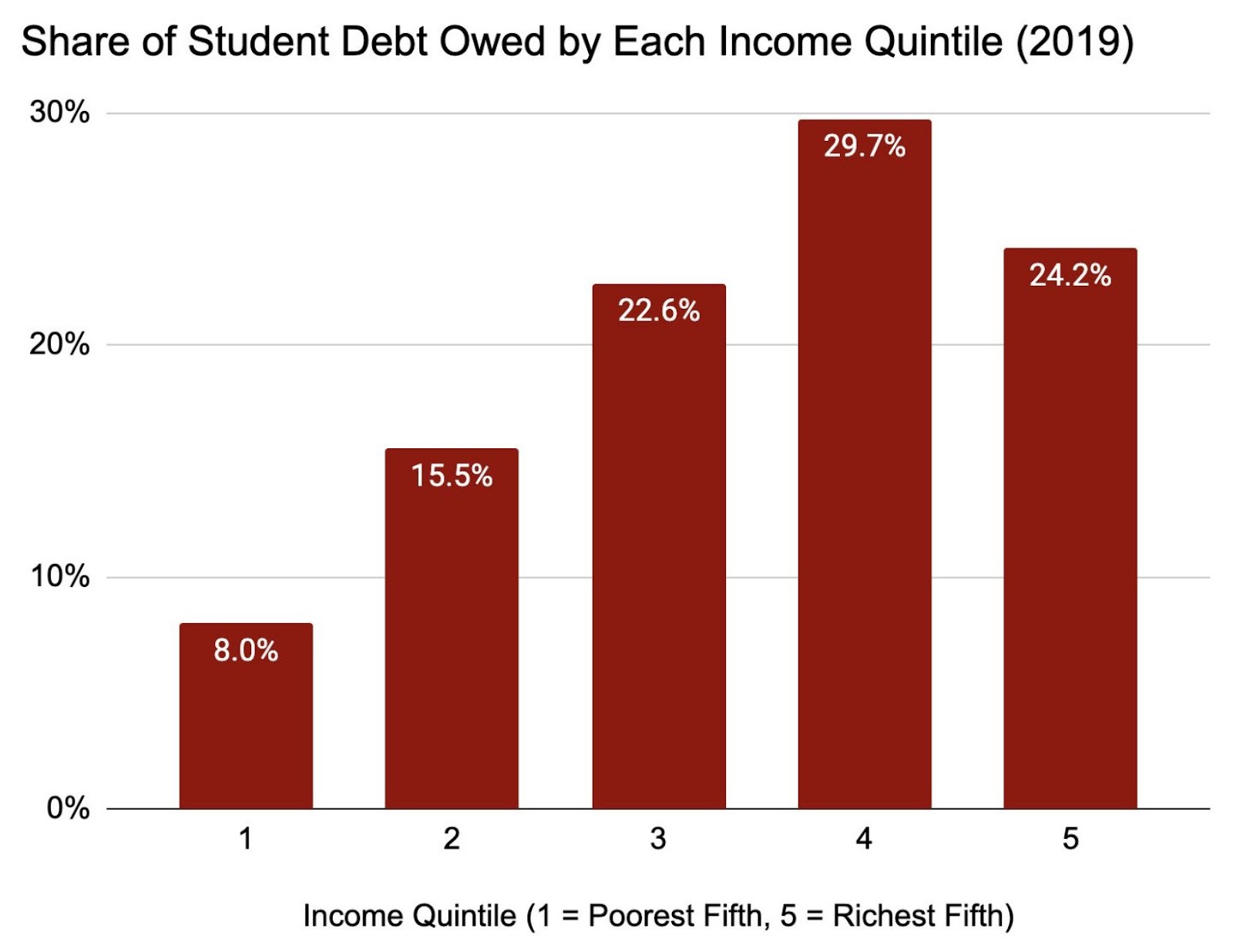

The currently popular idea is loan forgiveness of $10,000 for borrowers making less than $125,000, which would alleviate some complaints about this being a regressive policy, favoring the upper-middle class. Although student loan debt is indeed clustered among the higher income earners:

Other benefits center around racial equality, increasing homeownership, and simply being a quick and easy executive decision. This Atlantic article has some great supporting links to read more.

Unfortunately, you can choose which stat you want to argue for or against student loan forgiveness. That fact alone may mean we should cancel $10k for everyone because it sounds better than nothing.

Readers, I regret to inform you that I give a shit.

My problems aren’t anything that has already been listed (full disclosure: I already paid off my loans) but rather the lack of thought into the solution.

What about the university setting has changed over the last 100 years? Sure, the tech around college has changed, but what’s fundamentally different? You’re still sitting in a room while a person talks at you, and then you get tested on how well you listened.

College tuition costs have expanded at nearly three times the rate as the general level of CPI since 1978. So, yes, while a bachelor’s degree remains the surest way to set a floor on your salary, the cost to obtain the bachelor’s degree is out of control.

The pandemic has made people aware of something that has been true for a while. We need people with trade degrees with real, practical skills. And, of course, Reddit was there to make fun of this idea.

Student loan forgiveness doesn’t solve the labor force imbalance, nor does it hold universities accountable for driving everyone to a degree they didn’t need for the low, low price of $30k/yr.

Instead of canceling student loan debt, cancel the interest on student loans. Why in the actual F%#K do students have to pay high interest on loans that they can’t even declare bankruptcy on?

Again, federal student loans are not eligible for bankruptcy protection, and most loans originated before 2013 carried a 6.8% interest rate while bank accounts were paying 0%. Since then, they have cut us some slack, and loans that started between 2013 and today are in the range of 2.75% and 5.05% for undergrad.

So here’s an idea for the brain geniuses in the White House…

MAKE THE INTEREST ON STUDENT LOANS 0%

Stop making money on these things since you clearly don’t care if you are going to forgive debt anyway.

Simple rule, as long as you make payments (or have a legitimate reason to freeze them) the interest rate is 0%.

This way people have to pay back their debts (you’re welcome boomer), solving the moral hazard issue, while also removing the “charity” tagline from complete forgiveness. And we even have some proof that this works due to the moratorium on student loans during the pandemic. One estimate (by a site against student loan forgiveness) estimates that the average borrower saved $5,500 simply by freezing interest on loans over the last several years.

What’s the Upside?

Politics, especially when it comes to money, tend to be very contentious. But in our view, we have a simple solution to solve the student loan issue. Simply make the interest rate 0% on federal loans as long as you make payments.

This solves most popular arguments and makes the extremes on both sides unhappy which is usually a good sign in any negotiation. The power of compounding can not only help you save for retirement, but by removing it from student loans, it can help solve that crisis as well.

For Your Weekend

Our round-up of essays, podcasts, and streaming shows to check out over your weekend. We cast a wide net so you don’t have to.

Read:

Opinion: Canceling Student Loan Debt Is a Terrible Idea by Brian Riedl (The Dispatch)

The student loan “crisis” is primarily a manifestation of the progressive bubble—young, urban, college-educated professionals who are dealing with the high cost of rent, child care, and student loans. This includes the legislative and campaign staff of progressive politicians (and sometimes the politicians themselves!), who surely see their own self-interest in framing their personal finances as a crisis. Outside this bubble, student loan repayments are most often a manageable annoyance.

Opinion: Climate Catastrophists Need to Chill by Mona Charen (The Bulwark)

The Supreme Court building plaza was clear on April 22, Earth Day, when Wynn Bruce of Boulder, Colorado sat down next to a fountain. At 6:30 that evening, he set himself on fire, and though police were able to douse the flames, he later died of his injuries. His friend, climate scientist Kritee Kanko of the Environmental Defense Fund, explained that “This act is not suicide. This is a deeply fearless act of compassion to bring attention to [the] climate crisis.”

Big Money Donors Have Stepped Out of the Shadows to Create ‘Chaotic’ NIL Market by Ross Dellenger (Sports Illustrated)

Across the U.S. college sports landscape, from the heartland of Texas to the shores of Florida and hills of Tennessee, high-level boosters are privately or publicly using name, image and likeness deals to bankroll their teams, attempting to outbid one another for talent and creating a new arms race in college sports.

Chuckle: